If you’re age 50 or older, you’ve probably heard of “catch-up contributions.” It’s the IRS saying, “You are making more money, maybe those expensive kids are launched, go ahead and pile on the retirement savings. We’ll let ya.”

Up until this year, you could also protect those extra contributions from current income taxes. But, as I always say, the IRS Giveth; the IRS Can Taketh Away.

Starting in 2026, if you made over $150,000 in 2025, your catch-up contributions to your 401(k) must go into a Roth account. That means you pay taxes on that money now instead of later.

Oh and, and under the Giveth category, now there is a new Super Catch-Up for folks aged 60-63. Why not age to age 65 when Medicare starts and the age most people think they will retire? That would make too much sense for a government program.

Is this a tragedy? Maybe not.

The Good Stuff 👍

First, Roth money grows tax-free. That means when you retire and start using it, you won’t owe taxes on it. Future you might want to send present you a thank-you card.

Second, it gives you tax variety. Some of your savings will be taxed now, some later. It’s like having both chocolate and salted-caramel-Oreo ice cream. Nice to have options.

Third, no required withdrawals later for Roth 401(k)s (eventually, under newer rules). Translation: the government won’t force you to take money out on their schedule.

The Downside 👎

You have to pay taxes now. That can sting, especially if you were enjoying lowering your tax bill with traditional contributions.

Also, less flexibility today. Your paycheck might feel a little smaller, which is never anyone’s favorite surprise.

And honestly, it’s just… more complicated. Retirement was already confusing enough without plot twists.

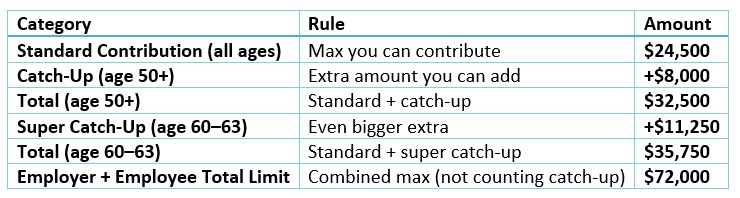

To help clarify, here is a handy chart for 2026:

So, Should You Still Do It?

In many cases, yes. If you can afford the taxes now, tax-free money later is a pretty sweet deal. But if cash is tight, you might need to rethink how much extra you put in.

Bottom line: The Catch-up (and its cousin Super) contribution is still a good tool. It may be forcing some tax diversification on you that you should have considered anyway. Roth contributions are less painful than Roth conversions, so we can choose to look at the bright side of this new rule.