An element of retirement income planning that never ceases to confuse is taxes.

Accounting for your tax bill as a retirement expense is important. Over-or-under estimating the cost can lead to errors in a retiree’s monthly spending targets.

The biggest misconception is that your marginal tax bracket is the amount you pay on all of your income. For example, “If I am filing Single, earn $100,000/year, and am the 22% tax bracket, I pay $22,000/year in Federal income taxes.”

That’s not how it works. We have tiered tax rate, so the first dollars of income you earn are taxed at 0%, the next tier at 12%, and on up.

It’s confusing to figure out your Real (or Average) tax rate, but this is an important number to know, especially for retirees.

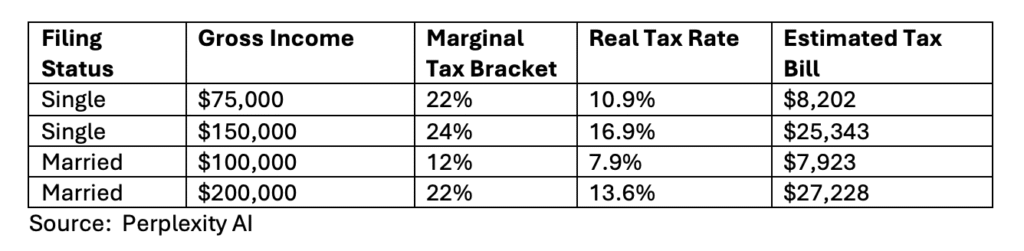

To give you some context, here are a few examples of incomes, marginal tax rates, and real tax rates.

Knowing your tax bill is a moving target, especially in the first years of retirement. There may be part time work, partial years worked before full retirement, or vacation or other benefits paid out in the early years.

Trying for an accurate place holder for your tax bill could allow you to spend more money on fun stuff and less anticipating a whomping tax bill that never materializes.